Approach

Markets continuously price performance, while constraints accumulate outside the price.

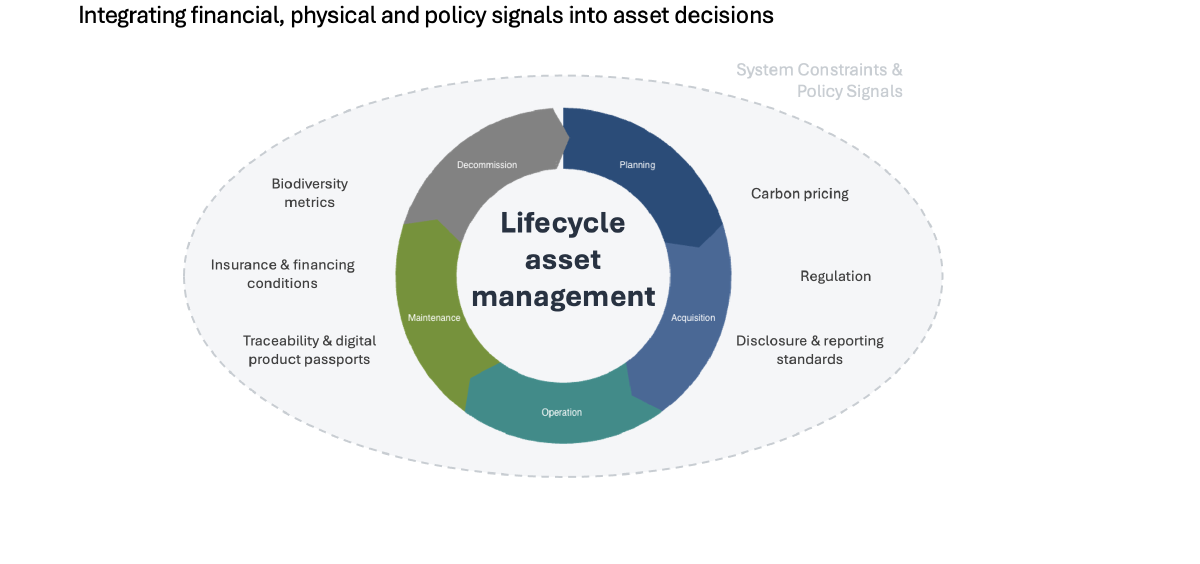

The diagram below sets out how I think about lifecycle asset management under system constraints. The five lifecycle phases (planning, acquisition, operation, maintenance, decommission) are each affected by the same enveloping set of signals: carbon pricing, regulation, disclosure and reporting standards, traceability and digital product passports, insurance and financing conditions, biodiversity metrics. Investment decisions taken in any one phase need to anticipate how each of those signals will evolve across the asset’s remaining life.

Behind that diagram sits a structural observation: investment decisions operate on three quite different time horizons.

Financial markets price performance on relatively short horizons. Expectations of revenues, costs and returns are repriced continuously as new information arrives.

Physical assets, however, operate on engineering horizons: technology cycles, efficiency curves, maintenance regimes and operational lifetimes that often stretch several decades. Aircraft, industrial plants, buildings and infrastructure assets purchased today are expected to remain operational well beyond 2050.

System constraints — carbon budgets, ecosystem capacity, resource depletion — operate on threshold horizons longer still. They are not continuously priced. They become visible through policy instruments that translate physical pressure into financial incentives, and through episodes of disorderly repricing when those instruments lag the underlying reality.

The work I do sits at the integration of these three horizons. The discipline is recognisably actuarial: managing the mismatch between assets and the liabilities, constraints and obligations they will encounter over their full life. What is new is the constraint class — physical and policy, rather than purely financial — and the asset class, which is increasingly real rather than financial.