Lifecycle asset management must now integrate financial, physical and policy signals simultaneously.

Extending actuarial thinking beyond insurance and financial portfolios, toward modelling how system constraints translate into investment decisions in the real economy.

This is an independent research and modelling initiative. The work is exploratory and ongoing — not a commercial product or consultancy offering.

For decades, financial markets have developed increasingly sophisticated tools to manage uncertainty within portfolios. As an actuary I have seen, and participated in, the rollout of frameworks such as Asset Liability Management and stochastic modelling, which brought a strong element of science into institutional investment decisions.

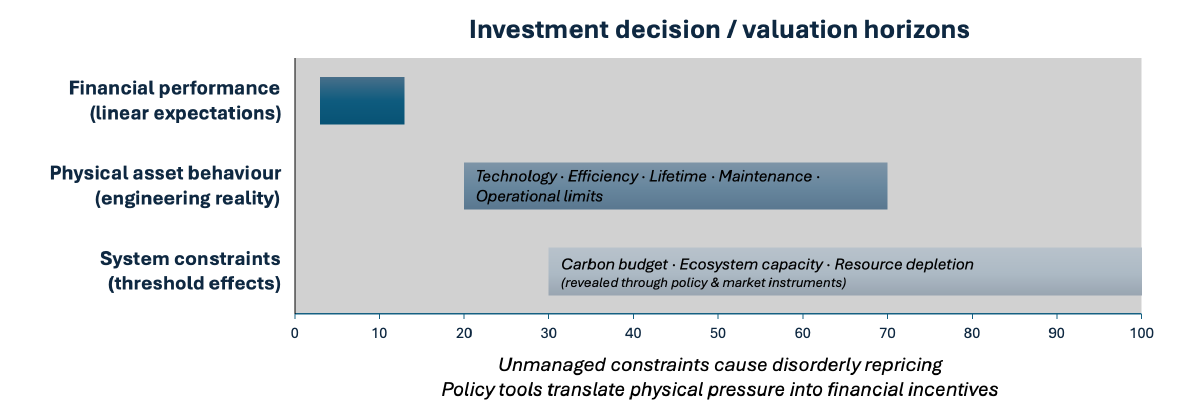

The challenge now extends beyond markets themselves. Assets increasingly operate within physical systems where constraints accumulate over time: carbon budgets, ecosystem capacity, resource availability. These pressures are progressively translated into financial incentives through policy instruments — most visibly through carbon pricing, but increasingly also through biodiversity metrics, disclosure standards and other regulatory frameworks.

These developments explain the growing importance of traceability and data infrastructures such as Digital Product Passports, which allow the lifecycle impact of assets and materials to be measured and integrated into decision-making.

In practice this means lifecycle asset management must now integrate financial, physical and policy signals simultaneously. For those of us working in actuarial science and quantitative risk modelling, this opens an interesting frontier: extending actuarial thinking beyond the confines of insurance and financial portfolios, toward modelling how system constraints translate into investment decisions in the real economy.